CARBON ACCOUNTABILITY IN PRIVATE SECURITY

IDG Security successfully piloted the E-Ledgers Carbon Accounting framework in its security operations in Afghanistan, one of the world’s most challenging operational environments. This initiative demonstrates IDG’s commitment to treating environmental responsibility as a core operational imperative, moving beyond statements of intent to establish a concrete and actionable framework. It also represents a step forward in carbon emissions due diligence for the private security industry. By applying the precision of financial accounting to environmental management, IDG generated a first-pass estimate of emissions with unprecedented accuracy. The pilot suggests that rigorous, bottom-up carbon accounting is feasible and beneficial for similar private security companies (PSCs) operating in remote or unstable environments.

Afghanistan: A climate change crisis

Climate change has become a critical factor shaping the operational landscape in Afghanistan. Although the country contributes minimally to global greenhouse gas emissions, it faces severe consequences of climate disruption, including drought, water scarcity and the loss of agricultural livelihoods. These environmental pressures exacerbate poverty, displacement and local insecurity.

Between 2021 and 2024, nearly three million people in Afghanistan were displaced by natural-hazard events such as droughts, floods, heavy snow and avalanches, and in 2024 alone more than 500,000 internally displaced people were recorded.[i] The country experiences overlapping extreme events, with drought-affected areas, flash floods and heavy snowfall increasingly interacting, undermining resilience and presenting recurrent risks to communities.[ii] These hazards disproportionately affect the most vulnerable populations, with livelihoods reliant on rain-fed agriculture or pastoralism often collapsing during drought, while floods and snowstorms destroy crops, livestock and shelter.

For IDG Security, these environmental pressures directly impact personnel, clients and the communities in which it operates. Recognising this, the company has reframed environmental responsibility as an operational necessity rather than a peripheral concern.

The importance of carbon accounting

Carbon accounting, defined as the process of quantifying and reporting greenhouse gas emissions, has become a central pillar of responsible business practice across industries. Once considered a voluntary exercise, it is increasingly moving toward a regulatory requirement as governments introduce mandatory disclosure frameworks.[iii]

In 2024, the International Financial Reporting Standards (IFRS) Foundation and its International Sustainability Standards Board introduced new global benchmarks for corporate transparency: the S1 Sustainability-related Disclosure and S2 Climate-related Disclosure standards. These standards aim to create a consistent framework for how organisations measure and communicate their climate impacts. Many countries are now preparing to embed these principles into national reporting systems.[iv] For the private security sector, this shift reinforces the need for robust carbon accounting systems that can deliver reliable, auditable data to clients and regulators alike.

E-Ledgers carbon accounting

E-Ledgers, developed through a partnership between Professors Robert Kaplan and Karthik Ramanna and the E-Ledgers programme, represents a major methodological shift in how organisations measure and manage their carbon emissions. The system applies the logic of cost-based financial accounting to environmental impacts, enabling companies to track emissions with a degree of precision traditionally used in monetary transactions.[v]

Conventional reporting frameworks, such as those based on the Greenhouse Gas Protocol, rely heavily on broad averages, sector-level emission factors and estimated upstream impacts. As highlighted in a 2024 Harvard Business Review (HBR) article on the Afghanistan pilot, these limitations often lead to inconsistent reporting and an inability to verify supply-chain emissions with any real confidence.[vi] In complex operations, this lack of traceability can obscure the true sources of carbon impact and undermine efforts to manage emissions effectively.

E-Ledgers addresses these shortcomings by requiring companies to measure emissions at the point of origin and then allocate them throughout the value chain. By combining direct emissions data with supplier-reported figures, the method captures the embedded carbon in every input and assigns it proportionally to the products or services generated. This produces auditable, real-time data that mirrors the accuracy and traceability of financial ledgers.[vii]

This approach is especially valuable for organisations operating in environments where traditional assumptions about emissions sources do not hold. The HBR article notes that rigorous accounting often reveals unexpected drivers of a company’s footprint, such as food systems, life-support logistics or other non-fuel-related operations, areas that standard estimation models tend to overlook.[viii] The framework therefore shifts carbon accounting from a compliance-oriented exercise to a tool that can meaningfully inform operational decision-making.

For IDG Security, the relevance of E-Ledgers lay in its ability to produce reliable, bottom-up data even in the most challenging contexts. The system’s emphasis on supply-chain traceability, internal operational discipline and verifiable allocation rules aligned directly with IDG’s objective to establish an environmental accounting model that could withstand scrutiny from clients, auditors and regulators.[ix]

IDG’s Afghanistan pilot

IDG is among the first private security companies to pilot the E-Ledgers carbon accounting framework, conducting the initiative in Afghanistan, an environment with significant operational and logistical challenges. The pilot focused on measuring the carbon footprint of delivering security services to 35 UN sites across the country, providing a clear and measurable operational output.

To ensure accurate, bottom-up emissions accounting, the team examined every component involved in delivering these services. This included personnel recruitment and training, transportation and equipment provisioning, food supply and life-support systems, and corporate overheads such as IDG’s headquarters in Dubai. Procurement staff were trained to collect detailed supplier-level information, including the origin of food products, the use of fertilisers or pesticides, transportation modes and distances and delivery frequency, which is often difficult to capture in high-risk, remote environments.

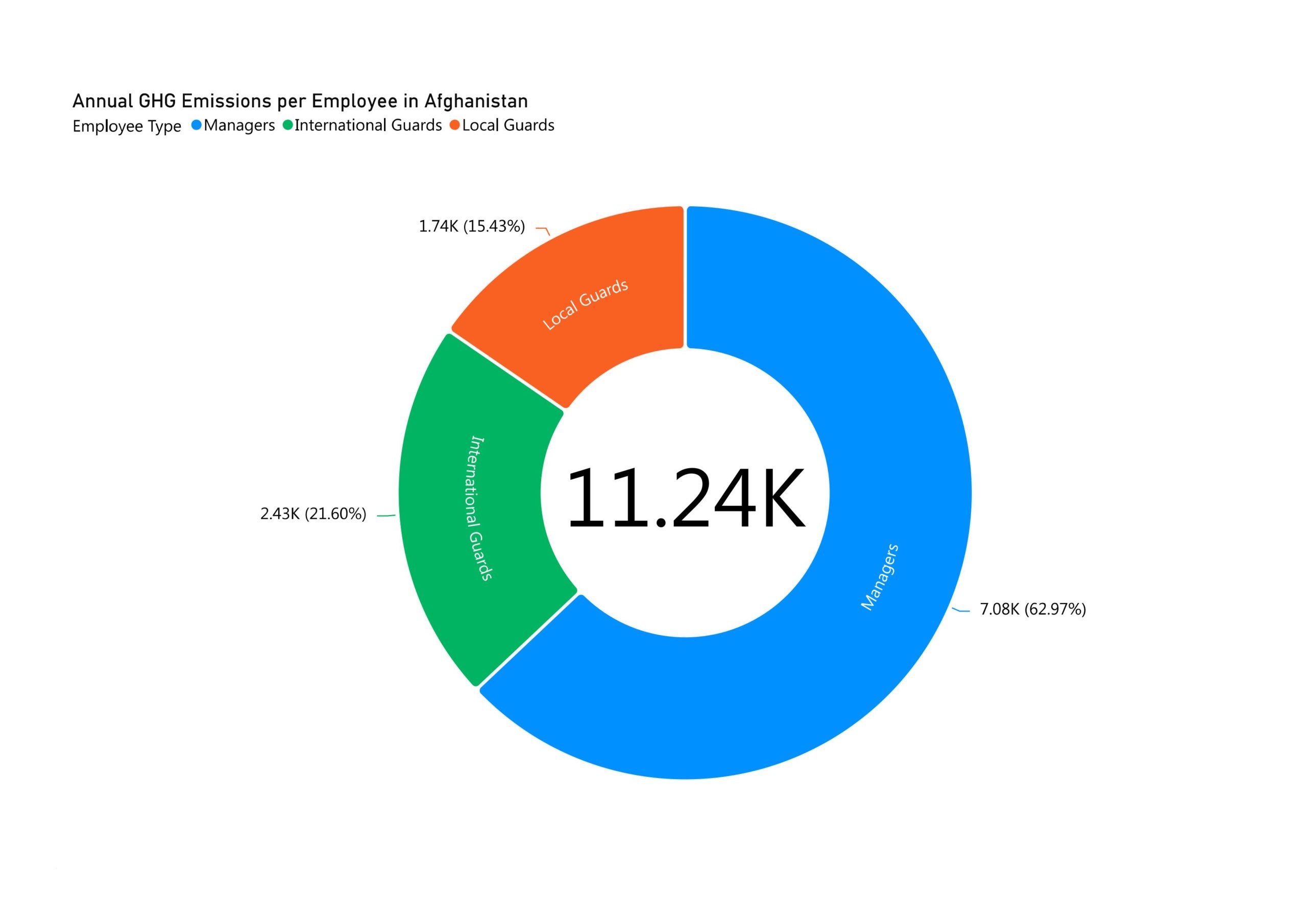

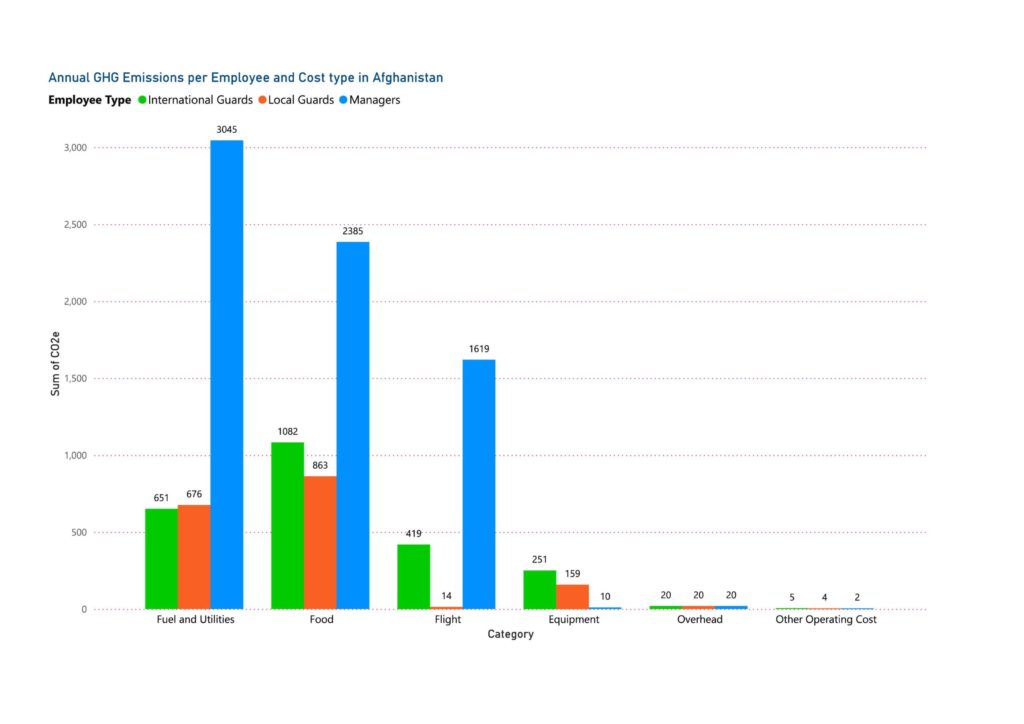

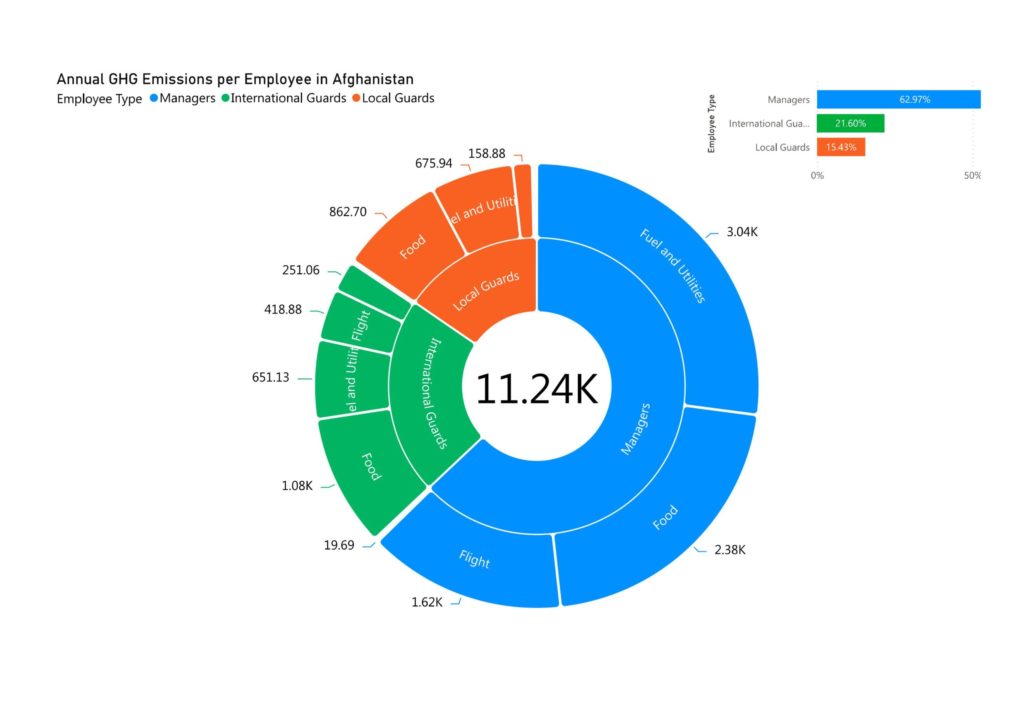

The assessment also considered differences between personnel groups, including Western ex-servicemen, Nepalese Gurkhas and local Afghan staff, reflecting variations in diet, accommodation, energy use and logistical support requirements. Western personnel had higher emissions associated with food and energy use, while local Afghan staff proved to be the most emissions-efficient on a per-service basis. The level of detail in this approach allows E-Ledgers to identify emissions sources that might otherwise be overlooked in complex service operations.

Evidence of impact

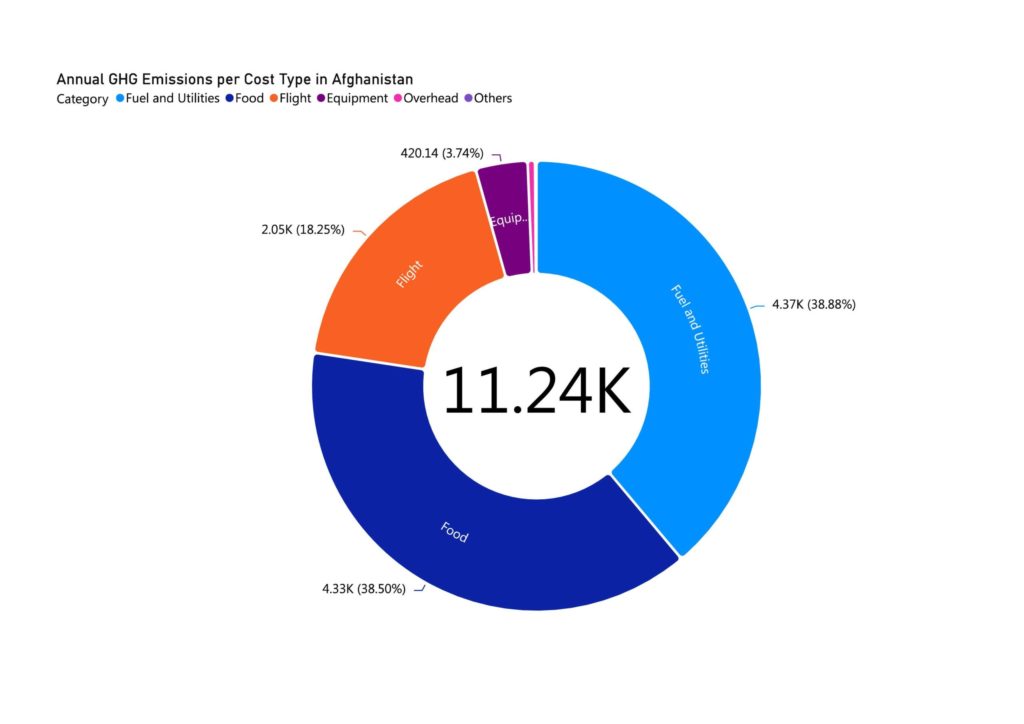

The E-Ledgers pilot revealed that food-related emissions were the single largest contributor to IDG’s carbon footprint, accounting for 38.5% of total emissions. This proportion exceeded emissions from transportation, fuel consumption and air travel for senior managers. The high level of food-related emissions reflected both the company’s provision of full life support for many on-site personnel and inefficiencies in local supply chains, including transportation, storage and handling of food.[x]

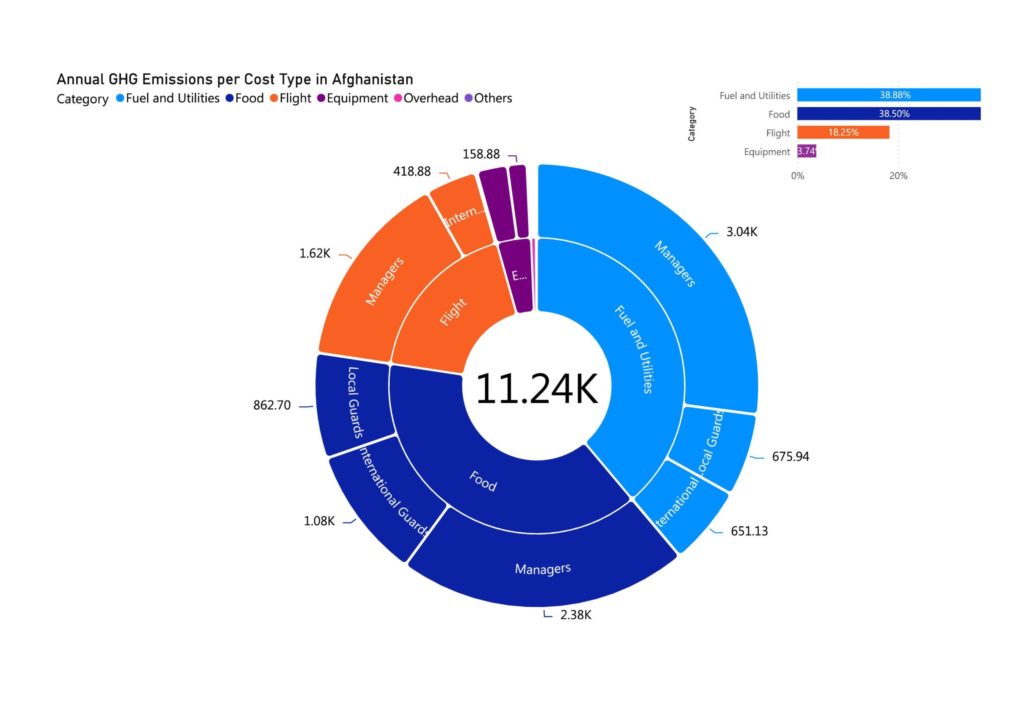

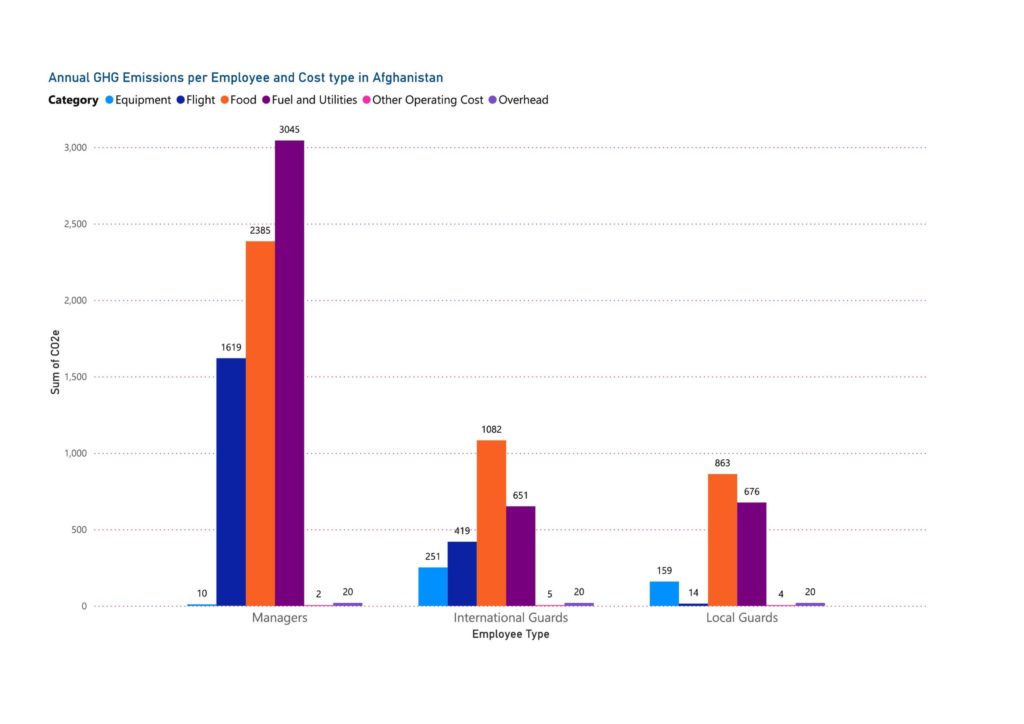

The E-Ledgers methodology made it possible to quantify emissions for each component of service delivery, from equipment use and training to headquarters overhead. This transparency allowed IDG to see where emissions were concentrated and identify actionable opportunities for reduction, turning abstract environmental metrics into operationally useful information.

The results highlighted the need to balance sustainability objectives with critical operational requirements. While the data identified opportunities for emissions reduction, decisions regarding staff nutrition, safety and morale could not be compromised without jeopardising mission-critical performance in a high-stress environment. Rigorous accounting supports operational decision-making by revealing trade-offs and informing strategies that reduce emissions without undermining essentials.

Next steps

Following the initial pilot, IDG plans to refine its data-gathering processes to improve accuracy and efficiency. The company will also seek external verification of its emissions results to enhance credibility and transparency. Over time, this process is expected to enable IDG to implement targeted interventions, optimise supply chains and promote evidence-based sustainability practices across its operations. This model, if adopted more widely, could set a new standard for private security companies operating in high-risk environments, demonstrating that environmental responsibility and operational effectiveness are compatible goals.

Recommendations

IDG’s experience offers valuable guidance for other private security companies:

- Feasibility for similar PSCs: IDG’s experience suggests that the E-Ledgers methodology is practicable for other private security companies operating in comparable high-risk environments.

- Leverage internal expertise: Companies can use existing operational and accounting capabilities internally to achieve broad engagement and avoid costly reliance on external consultants.

- Challenge assumptions: Rigorous, bottom-up data collection is vital as it challenges prior assumptions and uncovers unexpected emissions sources, such as supply chain inefficiencies, that might otherwise remain hidden.

- Promote transparency: Full transparency is essential. Sharing audited carbon accounts with clients allows them to make procurement decisions based on verifiable data, fostering trust and encouraging responsible supplier selection.

- Supplier collaboration: Accuracy improves when organisations collaborate with suppliers, and encouraging them to adopt the same methodology creates a cascading effect of accountability across the supply chain.

Conclusion

By embedding rigorous carbon accounting into its operational framework, IDG Security demonstrates that environmental responsibility can be systematically pursued alongside operational imperatives. The company is setting a standard for private security organisations operating in challenging environments, showing that actionable and verifiable carbon emissions data can be integrated into complex service operations. A clear example of this is IDG’s decision to include monthly CO₂ totals on invoices to its UN clients, making emissions reporting a routine and transparent part of service delivery. Its experience demonstrates that robust sustainability management is achievable when organisations are committed, innovative and prepared to measure and manage their environmental impact systematically.

Adopting the E-Ledgers approach allows companies to see their environmental footprint as a quantifiable metric rather than a vague cost. This transforms the abstract concept of climate impact into auditable and actionable data that informs strategic decisions on resource allocation and risk management, supporting both operational and sustainability objectives. IDG Security’s example highlights how a private security company can lead the way in combining operational excellence with environmental accountability, providing a model for the wider industry to follow.

Sources

Unless otherwise cited, information in this case study regarding IDG Security’s implementation of the E-Ledgers pilot in Afghanistan is drawn from personal communications with IDG staff in 2025 and 2026.

[i] International Organization for Migration. (2025, July). Data Update: Climate — Afghanistan. In DTM Insight July 2025 Edition. https://dtm.iom.int/dtm-insights/july-2025-edition/data-update-climate-afghanistan

[ii] Ibid.

[iii] Amel-Zadeh, A., & Tang, Q. (2025). Managing the shift from voluntary to mandatory climate disclosure: The role of carbon accounting. The British Accounting Review, 57(2), Article 101594. https://doi.org/10.1016/j.bar.2025.101594

[iv] Ibid.

[v] Kaplan, R. & Ramanna, K. “Accounting for Climate Change.” Harvard Business Review, Nov–Dec 2021.

https://hbr.org/2021/11/accounting-for-climate-change

[vi] Ramanna, K. “What Companies Can Learn from a Carbon Accounting Pilot in Afghanistan.” Harvard Business Review, October 7, 2024.

https://hbr.org/2024/10/what-companies-can-learn-from-a-carbon-accounting-pilot-in-afghanistan

[vii] Kaplan, R. & Ramanna, K. “Accounting for Climate Change.” Harvard Business Review, Nov–Dec 2021.

https://hbr.org/2021/11/accounting-for-climate-change

[viii] Ramanna, K. “What Companies Can Learn from a Carbon Accounting Pilot in Afghanistan.” Harvard Business Review, October 7, 2024.

https://hbr.org/2024/10/what-companies-can-learn-from-a-carbon-accounting-pilot-in-afghanistan

[ix] Ibid.

[x] Ibid.

Disclaimer

As per the Disclaimer on the homepage, neither the International Code of Conduct Association nor any authors can be identified with any opinions expressed in the text of or sources included in The International Code of Conduct Case Map.